In Nigeria, small businesses are stuck between a rock and a hard place when it comes to financing their dreams.

Traditional banks, once seen as a reliable lifeline for entrepreneurs, now seem more like gatekeepers, demanding collateral and endless paperwork, leaving many small to medium-sized enterprises (SMEs) high and dry.

As a result, a new breed of online lenders is stepping in, offering quick cash but at eye-watering rates that risk turning opportunity into a trap.

Key Points:

-

Traditional banks remain cautious, requiring collateral and complex documentation that many SMEs lack, despite years of banking relationships.

-

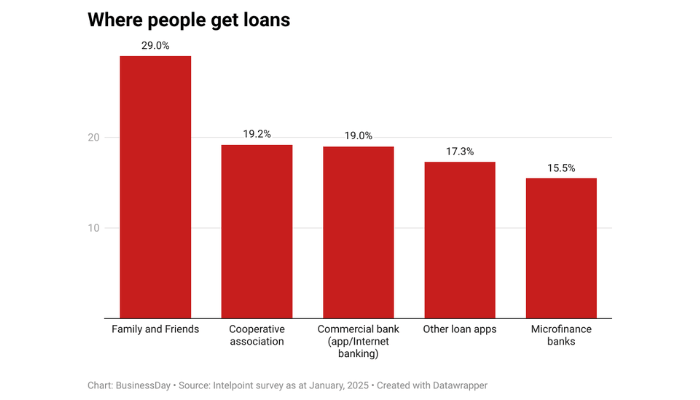

Entrepreneurs face monthly interest rates up to 58% from online lenders like Opay, Carbon, and Palmpay to keep businesses afloat.

-

Collateral requirements and risk frameworks exclude many SMEs from traditional bank financing, especially those in manufacturing and long-term production.

-

Banks prefer quick-return sectors like oil, gas, agriculture, and real estate, according to financial analysts.

-

SMEs lack knowledge of equity financing, highlighting an urgent need for education and outreach on alternative funding options.

-

Entrepreneurs call for a fairer, more inclusive credit system that recognises their potential and supports sustainable business growth.

Years of Banking, No Loans in Sight

BusinessDay highlighted the case of Ezenwammadu Buruzochukwu, CEO of Bewin Garments Industry and House of Bewin. For over a decade, he’s been loyal to Access Bank, diligently maintaining his business account. Yet, when it came time to expand his 3D polo shirt production, which churns out 5,000 shirts per week, the bank closed its doors. “They said I don’t have a Certificate of Occupancy,” he lamented. “Access Bank has shown me shege oooo.”

The consequence? He’s now hooked on online lenders like Carbon and Palmpay, which dispense cash instantly but at jaw-dropping interest rates — sometimes 58% per month. That means borrowing ₦1 million today means paying back nearly ₦1.6 million in just 30 days. Instead of building his business, he’s scrambling to service debts. “It’s like keeping my business alive, but not growing it,” he said.

His experience isn’t unique. Samuel Udeji, head of SAMUD Ventures Limited, which handles electrical contracts and supplies, is caught in the same bind. Despite maintaining an account with Zenith Bank for over 20 years, he’s never managed to secure a loan from them. “Zenith finances my clients,” he noted ironically, “but they won’t finance me.” For him, the relationship feels like a one-way street.

Banks Playing It Safe

Financial analysts argue that banks are simply protecting themselves. “Banks are in it for the bottom line,” said Yinka Awosanya of Businessfront Limited. “They want to know they’ll get their money back, and that’s why they demand collateral and strict documentation.”

Another analyst, Olumide Adesina, pointed to the numbers. “Non-performing loans have dropped from 4.3% to 3.8%, but banks are still reeling from FX devaluation. Some even got delisted due to bad loans,” he explained. This risk-averse mindset has led banks to cherry-pick sectors they consider safe bets: oil, gas, agriculture, and real estate.

“Each bank has its own risk appetite,” Adesina added. “It’s like approaching different cultures — you don’t approach an Igbo woman the same way you’d approach a Yoruba woman.” His point? Banks, too, have their own ‘cultures’ that dictate how they treat SME financing.

Paying More, Getting Less

For entrepreneurs, the choice boils down to this: wait months for a traditional bank loan that may never come, or click ‘apply’ on a loan app and pay through the nose. “Online lenders are fast, but they’ll drain you,” Buruzochukwu admitted. “They’re there for you, but at a heavy price.”

While digital loans keep businesses afloat in the short term, they’re not building long-term resilience. High interest rates eat into profits and leave entrepreneurs with little room to invest in growth, innovation, or new hires.

The Missing Piece: Equity

Beyond the debt trap, there’s another issue: many SME owners don’t know about — or feel equipped to pursue — alternative financing models like equity investment. When financial analyst Kalu Aja asked Buruzochukwu whether he’d considered selling shares to raise capital, the entrepreneur shook his head. “I don’t know how it works,” he admitted.

This lack of financial literacy around equity funding means countless promising businesses are missing out on opportunities to attract investors, share risk, and grow sustainably.

A System Stacked Against Entrepreneurs

Nigeria’s credit system is leaving many SMEs stranded. Traditional banks cling to caution while online lenders swoop in, charging rates that can easily bankrupt the very businesses they claim to serve. Meanwhile, the idea of equity financing remains a mystery to too many entrepreneurs.

If Nigeria is to unlock the potential of its small businesses — the lifeblood of its economy — then banks, regulators, and financial advisors must work together to bridge this financing gap. That means more than just offering loans; it means education, support, and real partnerships that put entrepreneurs back in the driver’s seat.

{kind=link}